January 26, 2012

- in Uncategorized by schooloftrade

Day Trading Strategies for Dollar Index , Euro, Crude, Russell and Gold futures

—————————————————————————————

The James’ Report: Day Trading Strategies for Professional Traders

—————————————————————————————

***Notes/Observations

from around the world***

from around the world***

–

Fed Chairman Bernanke signals years of low interest rates ahead with potential

more stimulus.

Fed Chairman Bernanke signals years of low interest rates ahead with potential

more stimulus.

– US Fed stance appears

to be pro inflationary

to be pro inflationary

–

Dow approaching 3 highs

Dow approaching 3 highs

–

US Tsy Sec Geithner will not participate in any Obama second term

US Tsy Sec Geithner will not participate in any Obama second term

–

Reports that private creditors were willing to accept a lower coupon in the PSI

negotiations

Reports that private creditors were willing to accept a lower coupon in the PSI

negotiations

– European equity

indices opened the session higher, as the US Fed disclosed that 11 out of 17 of

its members saw the FOMC raising the Fed funds rate in 2014 or later.

Ahead of the Fed meeting, there were expectations in the market that the Fed

would not raise rates until at least mid-2014. Since the open, indices have

continued to gain on renewed optimism related to the Greece private sector

involvement talks, after a Greek press report, without citing sources, said Greece’s

private lenders were said to be willing to accept a coupon rate of below 4% on

new Greek bonds. In the past, it was reported that Greece’s private lenders

were seeking a coupon of at least 4%.

indices opened the session higher, as the US Fed disclosed that 11 out of 17 of

its members saw the FOMC raising the Fed funds rate in 2014 or later.

Ahead of the Fed meeting, there were expectations in the market that the Fed

would not raise rates until at least mid-2014. Since the open, indices have

continued to gain on renewed optimism related to the Greece private sector

involvement talks, after a Greek press report, without citing sources, said Greece’s

private lenders were said to be willing to accept a coupon rate of below 4% on

new Greek bonds. In the past, it was reported that Greece’s private lenders

were seeking a coupon of at least 4%.

Speakers:

–

Greek Press report stated that private lenders were said to have accepted lower

interest rate in Greek PSI deal with creditors are said to be willing to accept

a coupon rate of below 4% on new Greek bonds. The report did not name sources,

but said private sector creditors would submit a new improved offer with an avg

interest rate of 3.75%. EU finance ministers had been seeking a rate of no more

than 3.5% and in the past private lenders said that they would not accept less

than 4%.

Greek Press report stated that private lenders were said to have accepted lower

interest rate in Greek PSI deal with creditors are said to be willing to accept

a coupon rate of below 4% on new Greek bonds. The report did not name sources,

but said private sector creditors would submit a new improved offer with an avg

interest rate of 3.75%. EU finance ministers had been seeking a rate of no more

than 3.5% and in the past private lenders said that they would not accept less

than 4%.

–

German Fin Min Schaeuble reiterated its view that European crisis must be

addressed at its source during an address to the Bundestag (lower house). He

noted that it was likely that German banks would hit capital goals in June and

could fill capital gaps without aid. The SoFFin was preventive medicine for

euro zone contagion.

German Fin Min Schaeuble reiterated its view that European crisis must be

addressed at its source during an address to the Bundestag (lower house). He

noted that it was likely that German banks would hit capital goals in June and

could fill capital gaps without aid. The SoFFin was preventive medicine for

euro zone contagion.

–

German Econ Min Roesler commented that the ESM rescue fund had ‘clear

borderlines’ and that there was no clear link with its funding and fiscal pact.

Germany was doing every thing possible to defend the Euro

German Econ Min Roesler commented that the ESM rescue fund had ‘clear

borderlines’ and that there was no clear link with its funding and fiscal pact.

Germany was doing every thing possible to defend the Euro

–

Senior German Official commented that Greece was not on the agenda at the Jan

30th EU Leader Summit and did not expect Troika report on second package for

Greece to be ready by then

Senior German Official commented that Greece was not on the agenda at the Jan

30th EU Leader Summit and did not expect Troika report on second package for

Greece to be ready by then

–

(ES) Spain Budget Min Montoro commented that Spain was in a recession and it

was worse than Europe’s

(ES) Spain Budget Min Montoro commented that Spain was in a recession and it

was worse than Europe’s

–

Russian Central Bank Deputy Ulyukaev commented that inflationary risks have not

disappeared and that conditions were not appropriate for an interest rate cut.

On the reserve currency issue, Russia might diversify into AUD assets in early

Feb

Russian Central Bank Deputy Ulyukaev commented that inflationary risks have not

disappeared and that conditions were not appropriate for an interest rate cut.

On the reserve currency issue, Russia might diversify into AUD assets in early

Feb

Currencies:

–

FX markets continued to digest the impact of the Fed’s extended zero policy

guidance from Wednesday. The overall

effect has seen a weaker USD coupled with renewed risk appetite and higher

commodity prices. The greenback was at one-month lows against the Euro and GBP

and two-month lows against the CHF.

FX markets continued to digest the impact of the Fed’s extended zero policy

guidance from Wednesday. The overall

effect has seen a weaker USD coupled with renewed risk appetite and higher

commodity prices. The greenback was at one-month lows against the Euro and GBP

and two-month lows against the CHF.

Political/

In the Papers:

In the Papers:

–

The Irish Independent confirmed that the EU Commission will ‘carefully

consider’ Ireland’s bid to cut the Anglo Irish Bank’s bailout costs. The ECB

said it is open to proposals to replace Anglo Irish Bank’s €30B promissory

note, or government IOUs for another instrument. Ireland is paying around 6%

(although it could be refinanced at 3% by the EFSF) on the outstanding €31B in

promissory notes, issued mostly to deal with the collapse of Anglo Irish Bank.

The Irish Independent confirmed that the EU Commission will ‘carefully

consider’ Ireland’s bid to cut the Anglo Irish Bank’s bailout costs. The ECB

said it is open to proposals to replace Anglo Irish Bank’s €30B promissory

note, or government IOUs for another instrument. Ireland is paying around 6%

(although it could be refinanced at 3% by the EFSF) on the outstanding €31B in

promissory notes, issued mostly to deal with the collapse of Anglo Irish Bank.

–

Iranian policy maker Emad Hosseini said lawmakers are finalizing a bill to stop

all oil trade with Europe. The FT reported that according to Hosseini, if the

plan is approved, the government will stop oil sales to Europe before the EU

begins its embargo. The bill could be taken up by parliament before Sunday. On

January 23rd, EU officials agreed to impose an embargo on Iranian oil,

including plans to ban Iran’s petrochemical shipments from May 1st.

Iranian policy maker Emad Hosseini said lawmakers are finalizing a bill to stop

all oil trade with Europe. The FT reported that according to Hosseini, if the

plan is approved, the government will stop oil sales to Europe before the EU

begins its embargo. The bill could be taken up by parliament before Sunday. On

January 23rd, EU officials agreed to impose an embargo on Iranian oil,

including plans to ban Iran’s petrochemical shipments from May 1st.

—————————————————————————————

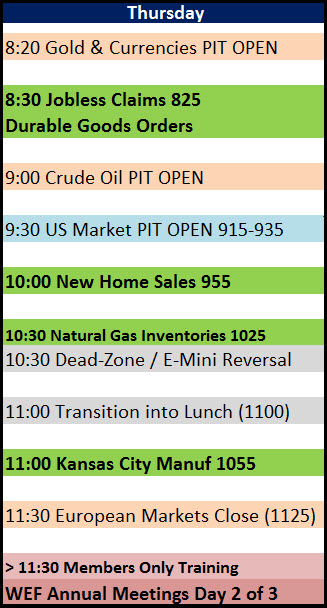

Today’s Economic News:

Our

day trading

strategies today will use the news, and this morning we have a

lot of action to prepare for. We begin

our day with the biggest news at 830am Jobless Claims and Durable Goods

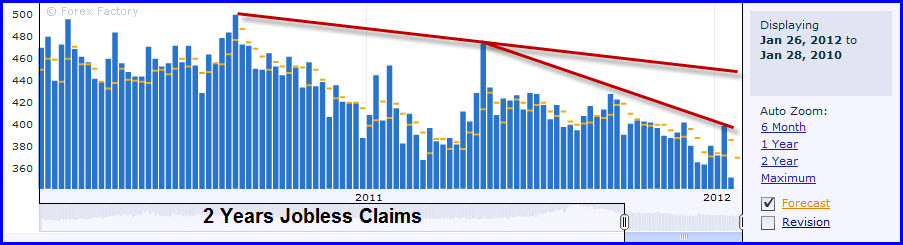

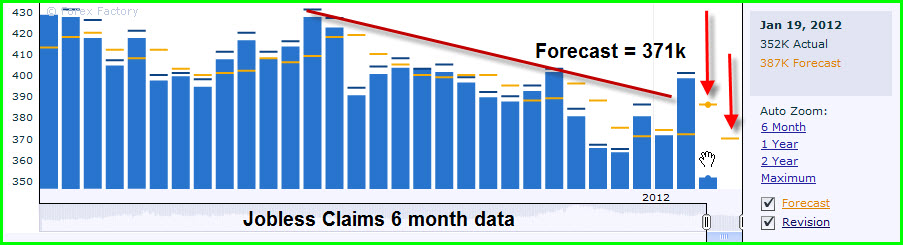

orders. You can see by the chart posted

below that there has been a steady downtrend in jobless claims over the long

term, but the recent 6 months data shows that 2 weeks ago we were much higher

than expected, and last week we were well below expectations. Both of the last 2 weeks of reports have shown

sub-400,000 in the report so they have been very strong, but today’s jobless

claims report will be a confirmation of this downward trend continuing. Now…if only there were some more JOBS along

with these lower ‘claims’ we would be in business for a recovery!

day trading

strategies today will use the news, and this morning we have a

lot of action to prepare for. We begin

our day with the biggest news at 830am Jobless Claims and Durable Goods

orders. You can see by the chart posted

below that there has been a steady downtrend in jobless claims over the long

term, but the recent 6 months data shows that 2 weeks ago we were much higher

than expected, and last week we were well below expectations. Both of the last 2 weeks of reports have shown

sub-400,000 in the report so they have been very strong, but today’s jobless

claims report will be a confirmation of this downward trend continuing. Now…if only there were some more JOBS along

with these lower ‘claims’ we would be in business for a recovery!

|

| Jobless Claims 2 years |

|

| Jobless Claims 6 months |

Looking

at the durable goods orders we can see a very strong correlation to the recent

manufacturing data here in the US. The

last 10 days we have seen nothing but strong manufacturing data, and this 6

months of Durable Goods clearly supports that we have more orders coming in and

more people headed back to work.

at the durable goods orders we can see a very strong correlation to the recent

manufacturing data here in the US. The

last 10 days we have seen nothing but strong manufacturing data, and this 6

months of Durable Goods clearly supports that we have more orders coming in and

more people headed back to work.

|

| Durable Goods 6 months |

Moving

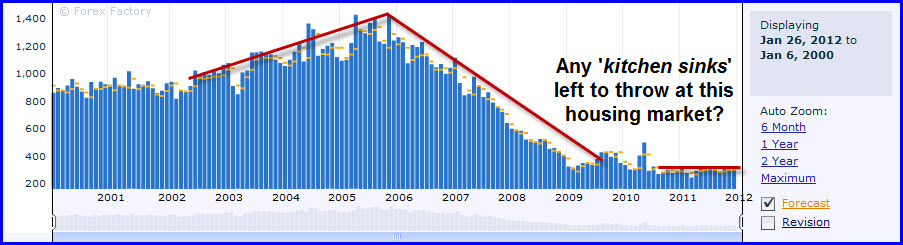

through the US Open at 930am EST we have New Home Sales at 1000am EST. This is considered to be a major news report among

professional traders, however, it wont move the market at all because none of

us TRUST this report right now. Too many

inflated figures and ‘window-dressing’ used to spice-up the housing market so

these numbers aren’t tremendously useful, used mostly as background noise to

support other claims to the economic changes in the US. We can see from the chart below that our New

Home Sales are at 10 year lows, and not looking very promising at this time considering

we have very little stimulus left in the bank to keep it propped up.

through the US Open at 930am EST we have New Home Sales at 1000am EST. This is considered to be a major news report among

professional traders, however, it wont move the market at all because none of

us TRUST this report right now. Too many

inflated figures and ‘window-dressing’ used to spice-up the housing market so

these numbers aren’t tremendously useful, used mostly as background noise to

support other claims to the economic changes in the US. We can see from the chart below that our New

Home Sales are at 10 year lows, and not looking very promising at this time considering

we have very little stimulus left in the bank to keep it propped up.

|

| New Home Sales 10 year |

At

1030am and 1100am today we have some minor news to be aware of. I marked them down because I wanted to know

when they were today, but they wont have much impact. Natural Gas Inventories are on our radar, but

unless you trade natty-gas you really don’t need to care much about it, and

Kansas City Fed is another manufacturing index that we like to watch because it

will further confirm/support the Empire State and Philly Fed manufacturing

numbers we saw last week, which were very strong suggesting growth in that

sector of the US economy.

1030am and 1100am today we have some minor news to be aware of. I marked them down because I wanted to know

when they were today, but they wont have much impact. Natural Gas Inventories are on our radar, but

unless you trade natty-gas you really don’t need to care much about it, and

Kansas City Fed is another manufacturing index that we like to watch because it

will further confirm/support the Empire State and Philly Fed manufacturing

numbers we saw last week, which were very strong suggesting growth in that

sector of the US economy.

Lets

also remember that today is day 2 of 3 for the WEF Meetings, which is open to

the press so we can expect to hear bits and pieces of news coming out of these

meetings today and tomorrow, so always on our toes today.

also remember that today is day 2 of 3 for the WEF Meetings, which is open to

the press so we can expect to hear bits and pieces of news coming out of these

meetings today and tomorrow, so always on our toes today.

This

morning we will be wrapping up with members-only after 1130am EST and we look

forward to working with members in training today, so bring questions and be

ready to learn!

morning we will be wrapping up with members-only after 1130am EST and we look

forward to working with members in training today, so bring questions and be

ready to learn!

|

| Day Trading News Strategy |

Please SHARE this resource with

friends, they want to learn this too!

friends, they want to learn this too!

—————————————————————————————

I use TradeTheNews.com for my live news data, and

I highly recommend it to all of my clients looking for this type of data. We have partnered with TTN to provide a FREE Trial

of this service by following this link: https://www.tradethenews.com/?affiliate=sot

I highly recommend it to all of my clients looking for this type of data. We have partnered with TTN to provide a FREE Trial

of this service by following this link: https://www.tradethenews.com/?affiliate=sot

I’m

always improving this prep, I appreciate your feedback, please post it here!