January 11, 2012

- in Uncategorized by schooloftrade

Day Trading Strategies for Dollar Index , Euro, Crude, Russell and Gold futures

—————————————————————————————

The James’ Report: Day Trading Strategies for Professional

Traders

Traders

—————————————————————————————

Around

the Globe this morning:

the Globe this morning:

–

European shares were trading in positive territory but failed to make any

impressive rally due to increasing concerns over the European debt crisis.

Germany’s first estimate of the Q4 GDP showed a contraction although Stats

office noted that 2012 domestic growth could remain robust. However, German

bond auction was well received, with a lower yield and higher bid-to-cover.

European shares were trading in positive territory but failed to make any

impressive rally due to increasing concerns over the European debt crisis.

Germany’s first estimate of the Q4 GDP showed a contraction although Stats

office noted that 2012 domestic growth could remain robust. However, German

bond auction was well received, with a lower yield and higher bid-to-cover.

– Germany heading towards a technical recession

–

German Chancellor Merkel hosts Italian PM Monti later today

German Chancellor Merkel hosts Italian PM Monti later today

–

Bank proposed Greek bond swap nears deal

Bank proposed Greek bond swap nears deal

–

Germany 5-year BOBL auction yield below 1.0% for the first time ever

Germany 5-year BOBL auction yield below 1.0% for the first time ever

– Mitt Romney wins US

New Hampshire Republican Party Primary

New Hampshire Republican Party Primary

Speakers:

–

Germany’s Stat Office commented that German economy started 2012 on a weaker

step but domestic growth could remain robust in 2012

Germany’s Stat Office commented that German economy started 2012 on a weaker

step but domestic growth could remain robust in 2012

–

Spain’s new government said to force banks to cut the values of foreclosed

homes by as much as half as part of its plan to clean up lenders’ balance

sheets

Spain’s new government said to force banks to cut the values of foreclosed

homes by as much as half as part of its plan to clean up lenders’ balance

sheets

–

China Premier Wen reiterated the view that the global economic situation was

extremely complicated and that cooperation between US and China is beneficial

while confrontation hurt both countries

China Premier Wen reiterated the view that the global economic situation was

extremely complicated and that cooperation between US and China is beneficial

while confrontation hurt both countries

–

US Tsy Sec Geithner commented that he did have productive talks with Chinese

leaders and was encouraged by China’s growth trajectory. He also noted that

there has been encouraging signs of strength in US economy recently

US Tsy Sec Geithner commented that he did have productive talks with Chinese

leaders and was encouraged by China’s growth trajectory. He also noted that

there has been encouraging signs of strength in US economy recently

–

US Official commented that China did recognize its excessive reliance on

external demand

US Official commented that China did recognize its excessive reliance on

external demand

And

spoke about continued appreciation of the CNY currency

spoke about continued appreciation of the CNY currency

–

EU’s Rehn reiterated his view that might be only at the beginning of the end in

dealing with EU crisis but still had chance of resolving the crisis but bold

decisions were needed. He hoped to conclude discussions on new treaty in coming

weeks and added that a fiscal stimulus in Germany was not the answer the situation

in the Euro Zone. Confident that Greece would reach an agreement with its

creditors in the coming weeks and the country would remain a member of the EMU

EU’s Rehn reiterated his view that might be only at the beginning of the end in

dealing with EU crisis but still had chance of resolving the crisis but bold

decisions were needed. He hoped to conclude discussions on new treaty in coming

weeks and added that a fiscal stimulus in Germany was not the answer the situation

in the Euro Zone. Confident that Greece would reach an agreement with its

creditors in the coming weeks and the country would remain a member of the EMU

Currencies:

–

FX markets were quiet for the majority of the European morning ahead of the

Sarkozy-Lagarde and Merkel-Monti

meetings in Paris and Berlin. Dealers did note that overnight weakness in

EUR/USD still appeared reluctant to test immediately lower and was vulnerable

to any headline excuse for to rally. The

pair did remain within is recent hourly range

FX markets were quiet for the majority of the European morning ahead of the

Sarkozy-Lagarde and Merkel-Monti

meetings in Paris and Berlin. Dealers did note that overnight weakness in

EUR/USD still appeared reluctant to test immediately lower and was vulnerable

to any headline excuse for to rally. The

pair did remain within is recent hourly range

Political/

In the Papers:

In the Papers:

– The FT reported that there are signs that

the strains in the European funding markets are easing. The benchmark

short-term EU bank lending rates (3-month Euribor) have declined for 14

straight sessions. In addition, the extra premium EU banks must pay to swap

Euros into US dollars has hit the lowest level since late October. This

suggests the ECB’s three-year lending program has helped improve money market

conditions.

the strains in the European funding markets are easing. The benchmark

short-term EU bank lending rates (3-month Euribor) have declined for 14

straight sessions. In addition, the extra premium EU banks must pay to swap

Euros into US dollars has hit the lowest level since late October. This

suggests the ECB’s three-year lending program has helped improve money market

conditions.

–

The concerns among euro zone government officials that Greek bailout costs

could eventually rise is one of the factors which has slowed the debt talks.

There are concerns that EU governments might have to refinance Greece until the

country is able to return to the markets.

The concerns among euro zone government officials that Greek bailout costs

could eventually rise is one of the factors which has slowed the debt talks.

There are concerns that EU governments might have to refinance Greece until the

country is able to return to the markets.

–

Certain Spanish banks are developing more properties, despite the declines in

housing prices. There are concerns that the moves to develop additional

properties could worsen Spain’s property glut. Certain banks have been

refinancing loans to developers which are unlikely to be repaid in order to avoid

write downs. Some analysts believe that

Spanish banks have yet to markdown their property assets to realistic levels.

Certain Spanish banks are developing more properties, despite the declines in

housing prices. There are concerns that the moves to develop additional

properties could worsen Spain’s property glut. Certain banks have been

refinancing loans to developers which are unlikely to be repaid in order to avoid

write downs. Some analysts believe that

Spanish banks have yet to markdown their property assets to realistic levels.

–

The Telegraph reported that analysts at UBS have criticized the Bank of England

(BoE) for not having an emergency support plan for the banking system. The

analysts believe that the lack of a backstop for the banking sector has already

led to higher funding costs for UK banks. Some British banks are paying more to

issue debt than their EU peers.

The Telegraph reported that analysts at UBS have criticized the Bank of England

(BoE) for not having an emergency support plan for the banking system. The

analysts believe that the lack of a backstop for the banking sector has already

led to higher funding costs for UK banks. Some British banks are paying more to

issue debt than their EU peers.

–

IMF inspectors returned to Ireland to ensure bailout conditions related to

€67.5 billion are met. The fifth report, expected to be completed by

mid-February, is to focus on the government’s reluctance to sell off many

state-owned assets and initiating deep financial sector reforms promised in

prior agreements. The IMF inspectors will meet with government ministers,

Central Bank, NTMA and various think tanks.

IMF inspectors returned to Ireland to ensure bailout conditions related to

€67.5 billion are met. The fifth report, expected to be completed by

mid-February, is to focus on the government’s reluctance to sell off many

state-owned assets and initiating deep financial sector reforms promised in

prior agreements. The IMF inspectors will meet with government ministers,

Central Bank, NTMA and various think tanks.

—————————————————————————————

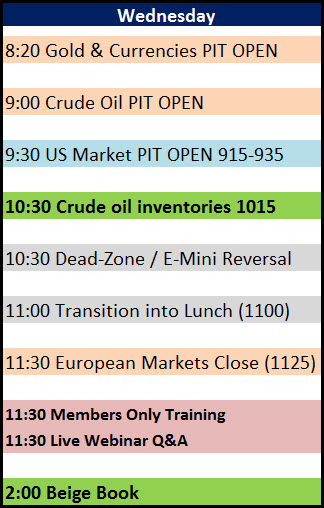

Today’s Economic News:

Our

day trading

strategies today will depend on the news, and this morning the

most important news we have is comes from crude oil futures and the inventories

data to be released at 1030am EST today.

This week has been slow because it’s the first week back from break for

many people, and today we should start seeing the rebound in volume and overall

consistency in the personality of the market.

day trading

strategies today will depend on the news, and this morning the

most important news we have is comes from crude oil futures and the inventories

data to be released at 1030am EST today.

This week has been slow because it’s the first week back from break for

many people, and today we should start seeing the rebound in volume and overall

consistency in the personality of the market.

The

key to day trading crude oil inventories is not to predict how the market will

react. Its often easy to anticipate ho w

the market will react to the news at 1030am however we need to be patient and

let the market as a WHOLE react to the news so we can follow along with the

move. Please note the Beige

Book news at 200pm EST may slow things down a little earlier than normal

today, considering it is a major news event.

key to day trading crude oil inventories is not to predict how the market will

react. Its often easy to anticipate ho w

the market will react to the news at 1030am however we need to be patient and

let the market as a WHOLE react to the news so we can follow along with the

move. Please note the Beige

Book news at 200pm EST may slow things down a little earlier than normal

today, considering it is a major news event.

|

| Click here to review crude oil inventories data |

—————————————————————————————

I’m

always improving this prep, I appreciate your feedback, please post it here!