- in Uncategorized by schooloftrade

Day Trading Strategies for Dollar Index , Euro, Crude, Russell and Gold futures

The James’ Report: Day Trading Strategies for Professional Traders

—————————————————————————————

and this morning remind ourselves that our success as traders is the sum of all

the little things we experience each day in the market. The little things we don’t notice, the small

victories and the minor obstacles along our journey, they all lead to growth as

a trader. Every day we trade is

significant, so don’t discount the value of TODAY’s price action, good or bad,

we will learn from it today.

from around the world***

|

| Heat Map Shows a Sluggish Morning |

European shares rallied lifted by a

stronger banking sector which is up following ECB’s LTRO allotment this week

and press reports that EU leaders may agree to provide capital faster to the

€500B permanent bailout fund.

the first two installment this year and complete the capitalization in 2015,

which is one year ahead of the schedule. Goldman Sachs also boosted the

financial sector by upgrading European banks to Overweight

is a plan B if the Greece debt swap fails

Fed’s Williams: More stimulus needed if recovery falters

Euro Zone Leaders pave way for EU decision on Greek bailout agreement

– China diversifies

away from USD

–

Germany MoM Retail Sales disappoints

–

Spanish Feb Net Unemployment climbs more than expected

The European fiscal compact was signed by 25 EU leaders. EU’s President Van

Rompuy stated that the measure would restore trust among EU states

Germany Econ Min: Roesler commented in the German press that the supported the

idea of placing a European Commissioner in charge of economic development in

Greece but could not understand Greek

objections to the proposal. He observed that the Greek people were aware of the needed

sacrifices, but the Greek elite did not want to give up their privileges.

BOJ Yamaguchi commented that the central bank might need new tools for its 1%

CPI target and was flexible and ready to move if necessary. He noted the BOJ

was not thinking about unwinding measures nor saw the need at this time to

extend JGB period under program

Japan Public Pension Fund (GPIF) (world’s largest) reported its Oct-Dec qtr

returns which rose by 0.58% compared to a prior loss of-3.32% q/q. It noted

that it’s posted a profit of ¥618.7B due to returns on foreign stocks. Assets

at Jan end to head down to ¥108.1T.

S&P EMEA managing director Fernandez de Heredia commented that Italy could

return to an ‘A’ rating if country moved in the right direction regarding its

debt, its growth and reforms. The first step by the rating agency would entail

a change of Italy’s outlook from negative to stable which depended on the debt,

growth and the economic impact of the reforms of PM Monti’s government. If

Italy goes in the right direction, S&P wouldl take this first step. The

recent decrease seen in govt’ yields were not enough for the outlook to change,

only sustainable impact of the reforms on growth can change the outlook

Japanese purchasers seek force majeure clause in the event it was unable to pay

Iran, or lift Iranian crude for lack of ship insurance coverage

Leaders were waiting for the final outcome of the Greek PSI swap on March 9th

and weaker German retail sales data pressured the EUR/USD from the getgo of the

session. The record amount of deposits in the ECB’s facility seemed to mirror

the net new borrowing from the recent 3-year lending LTRO and prompted concerns

whether bank would actually lend to assist the real economy.

The EUR/USD tested 1.3240 before stabilizing in the session but was off some

505 pips from its Asian opening levels.

Political/ In the

Papers:

The FT commented on concerns in Germany about the growth of the Bundesbank’s

balance sheet. The state bank’s Target2 balance is about €500B, which reflects

the amount that the German central bank has lent to the ECB. According to

Commerzbank, Target2 claims are the largest part of the Bundesbank’s balance sheet.

As a reminder, Target2 is the joint gross clearing system of the ESCB that

unifies the technical infrastructure of the 26 central (note-issuing) banks of

the EU.

Prosecutors in Germany raided various properties across Europe as part of an

insider trading probe related to allegations that certain investors tried to

inflate prices for penny stocks. German officials raided 53 properties in

Germany and inquired about 29 other sites outside of Germany.

The Telegraph’s Ambrose Evans-Pritchard suggested that the recent European

unemployment data shows a widening prosperity gap between the Northern and

Southern EU economies. SocGen analyst Klaus Baader believed the EU’s austerity

measures are having a more negative than expected impact on the EU’s labor markets,

particularly in the peripheral countries.

the G20 ministers last weekend in Mexico, it was recommended that the ECB lower

the target rate to less than 1% in addition to emergency loans to commercial

lenders. Monetary policy needed to be kept highly

accommodative, which the IMF said could be done by lowering the target policy

rate (where there is still room), and by more unconventional measures if

necessary.

—————————————————————————————

|

| New for Day Traders |

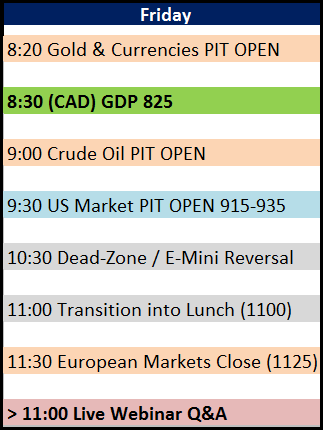

We

have a quiet trading day ahead of us this morning, without any real news on a Friday

we will look for a small window of opportunity from 830-1100am EST this morning

for the best volume and opportunity.

This morning is expected to be slower than normal because of the fact

that it is the first Friday of march, which usually has the jobs report, but today its only the 2nd day of the month so jobs report will be next Friday.

Summit in Brussels (all day)

–

(ES) Spain to present new budget targets

–

8:30 (CA) Canada Dec Gross Domestic Product M/M: +0.3%e v -0.1% prior; Y/Y:

1.9%e v 2.0% prior; Quarterly GDP Annualized GDP Y/Y: 1.8%e v 3.5% prior

– 9:45 (US) Feb ISM New

York: No est v prior

–

10:00 (DK) Denmark Feb Foreign Currency Reserves (DKK): No est v 492.6B prior

–

16:00 (CO) Colombia Feb Producer Price Index M/M: No est v -0.5% prior; Y/Y: No

est v 3.7% prior

–

20:00 (CN) China Feb Non-Manufacturing PMI: No est v 52.9 prior

–

20:00 (US) Fed’s Bullard speaks on U.S. Economy in Vancouver

—————————————————————————————

for my live news data, and I highly recommend it to all of my clients looking

for this type of data. We have partnered with TTN to provide a FREE Trial of this service by following

this link