- in Uncategorized by schooloftrade

Day Trading Strategies for Dollar Index , Euro, Crude, Russell and Gold futures

—————————————————————————————

value of picking up nickels and dimes throughout their day, month, and career. Every day is a new opportunity to learn more,

and the collection of lessons we learn from the markets every day may not

appear to have an immediate impact in your trading, but over time learning more

every day results in a well-rounded and confident trader. Find a way to learn more every day, and in

time you will see tremendous results.

|

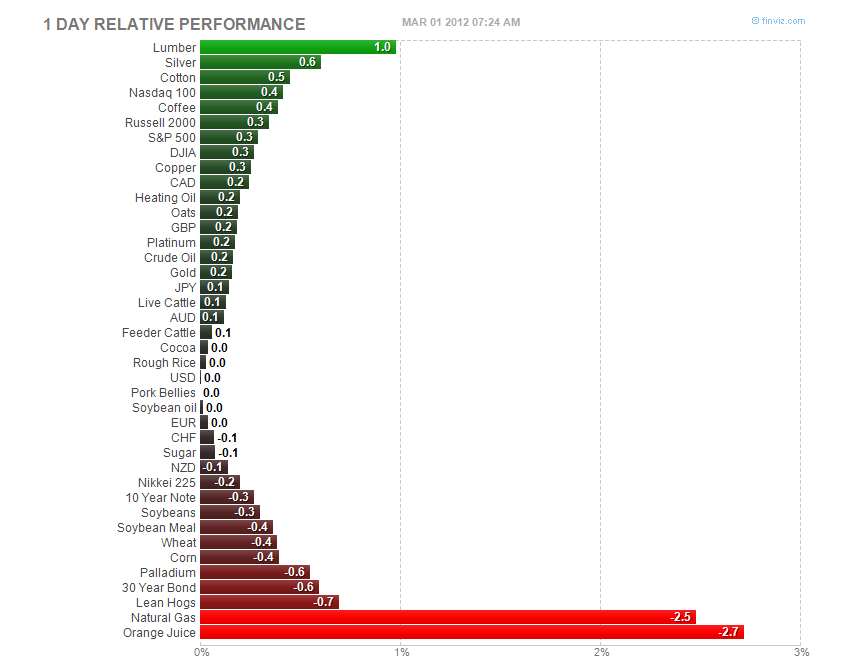

| Heat Map Futures |

world***

higher during the session even after FOMC’s minutes showed that the Fed was

not planning a second round of QE.

However, China and US PMI rose above expectations while jobless claims,

expected during NY morning, are expected at a four-year low.

provides no hint of QE3; has a change again today to clarify his views

Dealers note that ECB’s 3-year LTRO constitute an easing of monetary conditions

with €313B net add; ECB balance sheet now amounts to 32% of euro area GDP,

compared with 21% in the UK, 19% in the US and 30% in Japan

Italy 2-year Govt bond moves below 2.0% (first time since Oct 2010)

European PMI Manufacturing data mixed

Spain has completed almost 40% of gross 2012 issuance

Euro Zone Jan Unemployment Rate surges to record EMU levels

There were 2 questions said to have been asked to the ISDA about Greece’s

credit default swaps (CDS). The first question related to whether the use of a

collective action clause (CAC) was a credit event. – The second question

related to if the Greek debt swap represents a credit event. The ISDA meets

today with a decision expected before Monday, March 5th

ECB’s Makuch reiterated the central bank view of not expecting another 3-year

lending LTRO and that funds from second

LTRO to go to non-financials

Netherlands Bureau for Economic Policy Analysis (CPB) cuts 2012 and 2013 GDP

outlook. It trimmed the 2012 GDP view to -0.75% from -0.50% prior Dec forecast

and cuts its 2013 GDP view to 1.25% from 1.3% seen in Dec. The CPB also raised

the deficit to GDP for the period putting the 2012 Deficit at 4.5% from 4.1%

prior and the 2013 Deficit to GDP to 4.5% from 3.0% prior.

Brazil said to have raised IOF tax on some currency operations to curb BRL

strength (as speculated) – US financial press

BOE Miles: Aggressive loosening of monetary policy might help economy and make

it easier to normalize interest rates sooner. He noted that too much attention

has been paid to the impact of QE on gilt yields while focus on corporate

yields was more important. Low UK Govt bond yields were likely due to

safe-haven flows. He reiterates the view that inflation would likely keep

slowing

commented that there could be a slowdown in Asia as the Euro crisis and high

oil prices were a risk to the region’s growth outlook

Fed Chairman Bernanke lack of signal more policy stimulus continued to

aid the greenback during Asia today but entered into a

consolidation mode during the European morning. The European currencies were

off their morning lows and shock off a spat of mixed PMI manufacturing data and

a surge in the Euro Zone unemployment data.

The EUR/USD was trading around the 1.3340 leve and slightly positive from its

Asian opening level. The current resistance was seen at the 1.3365 level, which

was a former hourly support line earlier in the week.

The JPY currency maintained its soft tone. The USD/JPY remained above the 81

handle with EUR/JPY cross hovering around the 108 level.

Papers:

The Netherlands Bureau for Economic Policy Analysis (CPB) amended its economic

forecasts lowering its 2012 and 2013 GDP outlook. It cut the 2012 and 2013 GDP

view to -0.75% (-0.50% prior) and 1.25% (1.3% prior) respectively. Please see

our 01:43 head line for full the release.

Despite the ECB’s three-year LTRO operations conducted yesterday, there has

been only tepid demand for longer dated EU peripheral bonds. In terms of the

Italian yield curve, the two-year yields have declined more than 10-year

yields. The shape of the curve could mean that Italian bonds still have credit

risks.

The FT reported that the German Bundesbank continues to have concerns about the

ECB’s lending programs. In a letter to the ECB president, the head of the

Bundesbank Weidmann raised concerns about the risks related to the ECB’s

lending measures.

The Telegraph’s Ambrose Evans-Pritchard made positive and negative remarks

about the ECB’s LTROs. While the operation has lowered the risks of a credit

crunch, it has led to the EU’s weakest banks in increasing their holdings of

the sovereign debt of the weakest countries.

Germany’s Chancellor Merkel was said to have acknowledged international

pressure related to the limit for the ESM. According to the German press, which

cites government officials, the Chancellor could soften her opposition to

increasing the limit of the ESM to €750B from €500B. It was said that both the

ESM and EFSF could function simultaneously for about one year.

|

| News for Day Traders |

(US) Fed’s Pianalto

–

8:00 (BR) Brazil Feb PMI Manufacturing: No est v 50.6 prior

–

8:00 (US) Mar RBC Consumer Outlook Index: No est v 45.1 prior

–

8:00 (RO) Romania to sell Bonds

–

8:30 (EU) Poland Fin Min Rostowski speaks at Brussels Think

– 8:30 (CA) Canada Q4 Current Account

(BOP): -$9.6Be v -$12.1B prior

– 8:30 (CA) Canada Jan Industrial

Product Price M/M: +0.3%e v -0.7% prior; Raw Materials Price Index M/M: +0.5%e

v -2.4% prior

– 8:30 (US) Jan Personal Income: 0.4%e v

0.5% prior; Personal Spending: 0.4%e v 0.0% prior

– 8:30 (US) Jan PCE Core M/M: 0.2%e v

0.2% prior; Y/Y: 1.9%e v 1.8% prior; PCE Deflator Y/Y: 2.3%e v 2.4% prior

– 8:30 (US) Initial Jobless Claims:

355Ke v 351K prior; Continuing Claims: 3.415Me v 3.392M prior

– 10:00 (US) Fed Chairman Bernanke

delivers semi-annual monetary policy report

– 10:00 (US) Jan Construction Spending

M/M: 1.0%e v 1.5% prior

– 10:00 (US) Feb ISM Manufacturing:

54.5e v 54.1 prior; Prices Paid: 58.0e v 55.5 prior

–

10:00 (MX) Mexico Central Bank Economist Survey

–

10:00 (MX) Mexico Jan Remittances: $1.5Be v $1.8B prior

–

10:30 (US) Fed’s Raskin

–

10:30 (US) Weekly EIA Natural Gas Inventories

–

11:00 (IC) Iceland Q4 Current Account (ISK): No est v 12B prior

–

12:00 (FR) France Socialist Candidate Hollande to hold Meeting in Lyon

–

12:00 (IT) Italy Feb New Car Registrations Y/Y: No est v -16.9% prior

–

12:30 (US) Fed’s Lockhart speaks on Economy and Banking in Atlanta

–

13:00 (MX) Mexico Feb IMEF Manufacturing Index: 53.0e v 51.8 prior; Non-Manufacturing

Index: 52.9e v 51.7 prior

–

13:00 (BR) Brazil Feb Trade Balance: $2.3Be v -$12.9B prior

–

13:00 (IT) Italy Feb Budget Balance: No est v -€3.3Be; Budget Balance YTD: no

est v -€3.3B prior

–

15:30 (MX) Mexico Jan YTD Budget Balance (MXN): No est v -355.5B prior

–

17:00 (US) Feb Total Vehicle Sales: 14.00Me v 14.13M prior; Domestic Vehicle

Sales: 11.00Me v 11.05M prior

–

18:30 (JN) Japan Jan Unemployment Rate: 4.5%e v 4.6% prior

–

18:30 (JN) Japan Jan National CPI: -0.1%e v -0.1% prior

–

23:30 (US) Fed’s Williams speaks in Honolulu, HI

– (US) Republican Georgia Primary

Event

—————————————————————————————

for my live news data, and I highly recommend it to all of my clients looking

for this type of data. We have partnered with TTN to provide a FREE Trial of this service by following

this link